Australia's financial accountability regime is here—Are you ready?

08 September 2023

08 September 2023

FAR is near—the time to act is now

The incoming Financial Accountability Regime (FAR) will impose a stringent accountability framework for the directors and most senior executives of APRA-regulated entities. Across Australia, banks are working towards compliance by March 2024, with FAR applying to insurers and registrable superannuation entities from March 2025.

Given the dependencies required to support compliance with FAR, the time for banks, insurers and registrable superannuation entities to act is now.

Successful compliance with the regime will rely on understanding the complexity of FAR in the context of your entire business and aligning this with accountability across your accountable persons. Institutions will also need to remain cognisant of how regulators will use the data you provide now and in future.

How institutions identify accountabilities for a broad range of functions across end-to-end value chains and an often wide net of accountable executives is critical. Properly cascading responsibilities through all levels will set your governance, oversight, risk and compliance management frameworks apart.

Ultimately, an end-to-end, integrated approach to compliance with FAR obligations and other regulatory reforms will drive improved organisational and consumer outcomes.

Getting ahead of the next frontier of data-informed regulator collaboration—recognising how to deal with both the Australian Prudential Regulation Authority (APRA) and the Australian Securities and Investments Commission (ASIC) as joint administrators—will be critical to avoiding potentially far-reaching directions.

Cascading accountabilities through all levels of an institution as part of the BEAR and the United Kingdom's Senior Managers Regime has proven challenging — and has failed in some of the worst cases.

Institutions that are structured primarily by function have faced insurmountable obstacles in ensuring appropriate compliance with accountability regimes. This is particularly the case when attempting to map accountabilities across end-to-end value chains.

It is clear from the implementation of other accountability regimes that accountable entities will need to:

These steps will better position accountable entities to design and operate mechanisms that are suitable for their organisation and will also drive and demonstrate compliance.

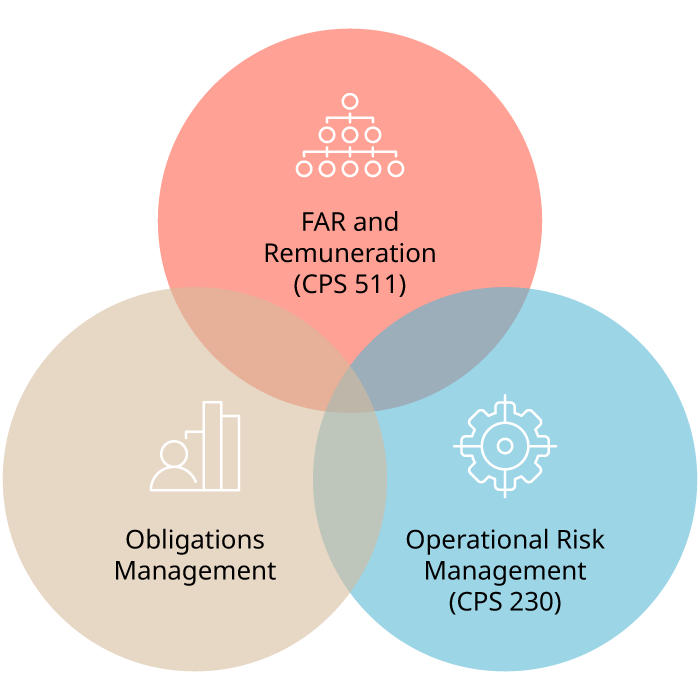

Most institutions will implement FAR at the same time as they continue to run their businesses and deliver risk or operating model transformation programs. This is alongside the concurrent introduction of inter-related key regulatory reforms that require an end-to-end view of the value chain, including remuneration (CPS 511) and operational risk management (CPS 230).

Execution risk in this context will need to be carefully managed. There will need to be a focus on dependencies and interoperability to ensure frameworks, systems, policies, processes and procedures are holistic, fit-for-purpose and sufficient for managing non-financial risks like compliance and conduct risks.

Understanding and implementing FAR in this integrated way will be a key differentiator for institutions looking to transition to, or implement, the new regime and translate it into practice as intended in a sustainable manner.

Both APRA and ASIC will administer FAR jointly, and those accountable entities subject to the regime should not expect a 'light touch' from the regulators. Rather, with increased signposting of focused enforcement approaches from both regulators, more proactive supervision, investigations and regulatory outcomes can be expected.

There are two key drivers for this shift:

In this environment, it is of fundamental significance that institutions refresh their regulatory strategies in a way that supports how accountable persons interact and engage with regulators.

Given the short implementation period, APRA-regulated institutions should embrace a multi-disciplinary approach swiftly. Bringing together legal, risk and business perspectives can quickly clarify how the legislation affects institutions, and translate this into implementing FAR in a compliant manner.

That's exactly how we help clients, with our unique integrated solutions and insights. Our legal-led consulting service brings together legal and risk expertise leveraging our extensive industry and regulatory experience, as well as our significant depth in advising financial services clients in Australia, to deliver proportionate, practical, defensible and sustainable solutions.

Reach out if you would like assistance, and we would be happy to help you on all aspects of the regime.

The Senate passed the Financial Accountability Regime Bill 2023 (Bill) on 5 September 2023, and the Bill is now awaiting Royal Assent. There were no changes to the Bill introduced earlier this year.

FAR imposes accountability obligations, key personnel obligations, deferred remuneration obligations and notification obligations.

As outlined in our previous article, Far is not far away, are you ready? :

While there are no individual civil penalties for accountable persons who breach their accountability obligations (other than in the case of being knowingly concerned in, or party to, a contravention of certain FAR provisions), it is important for accountable entities to undertake any framework uplifts where required, given ongoing regulatory scrutiny on accountability and potential civil penalties for accountable entities of more than double those under BEAR for large ADI (up to $210 million).

Authors: Miriam Kleiner, Partner, Legal Governance; Elizabeth Hristoforidis, Director, Risk Advisory; and Ethan Culross, Specialist, Risk Advisory.

This publication is a joint publication from Ashurst Australia and Ashurst Risk Advisory Pty Ltd, which are part of the Ashurst Group.

The Ashurst Group comprises Ashurst LLP, Ashurst Australia and their respective affiliates (including independent local partnerships, companies or other entities) which are authorised to use the name "Ashurst" or describe themselves as being affiliated with Ashurst. Some members of the Ashurst Group are limited liability entities.

The services provided by Ashurst Risk Advisory Pty Ltd do not constitute legal services or legal advice, and are not provided by Australian legal practitioners in that capacity. The laws and regulations which govern the provision of legal services in the relevant jurisdiction do not apply to the provision of non-legal services.

For more information about the Ashurst Group, which Ashurst Group entity operates in a particular country and the services offered, please visit www.ashurst.com

This material is current as at 8 September 2023 but does not take into account any developments after that date. It is not intended to be a comprehensive review of all developments in the law or in practice, or to cover all aspects of those referred to, and does not constitute professional advice. The information provided is general in nature, and does not take into account and is not intended to apply to any specific issues or circumstances. Readers should take independent advice. No part of this publication may be reproduced by any process without prior written permission from Ashurst. While we use reasonable skill and care in the preparation of this material, we accept no liability for use of and reliance upon it by any person.

The information provided is not intended to be a comprehensive review of all developments in the law and practice, or to cover all aspects of those referred to.

Readers should take legal advice before applying it to specific issues or transactions.